Compute one or more penalty values for a given omega, allowing

vectorized specifications of penalty, lambda, and gamma.

Arguments

- omega

A numeric value or vector at which the penalty is evaluated.

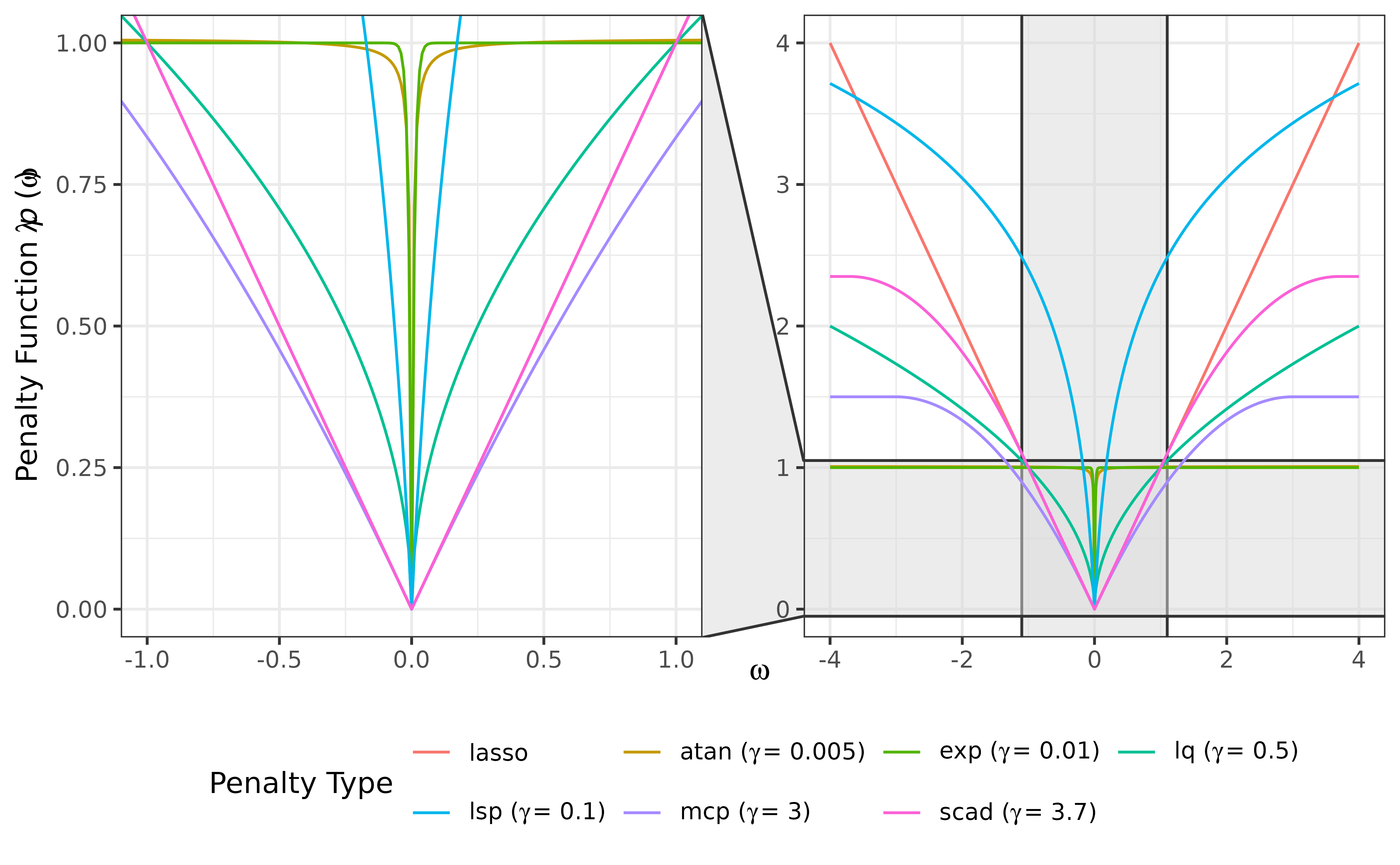

- penalty

A character string or vector specifying one or more penalty types. Available options include:

"lasso": Least absolute shrinkage and selection operator (Tibshirani 1996; Friedman et al. 2008) .

"atan": Arctangent type penalty (Wang and Zhu 2016) .

"exp": Exponential type penalty (Wang et al. 2018) .

"lq": Lq penalty (Frank and Friedman 1993; Fu 1998; Fan and Li 2001) .

"lsp": Log-sum penalty (Candès et al. 2008) .

"mcp": Minimax concave penalty (Zhang 2010) .

"scad": Smoothly clipped absolute deviation (Fan and Li 2001; Fan et al. 2009) .

If

penaltyhas length 1, it is recycled to the common length determined bypenalty,lambda, andgamma.- lambda

A non-negative numeric value or vector specifying the regularization parameter. If

lambdahas length 1, it is recycled to the common length determined bypenalty,lambda, andgamma.- gamma

A numeric value or vector specifying the additional parameter for the penalty function. If

lambdahas length 1, it is recycled to the common length determined bypenalty,lambda, andgamma. The penalty-specific defaults are:"atan": 0.005

"exp": 0.01

"lq": 0.5

"lsp": 0.1

"mcp": 3

"scad": 3.7

For

"lasso",gammais ignored.

Value

A data frame with S3 class "penalty" containing:

- omega

The input

omegavalues.- penalty

The penalty type for each row.

- lambda

The regularization parameter used.

- gamma

The additional penalty parameter used.

- value

The computed penalty value.

The number of rows equals

max(length(penalty), length(lambda), length(gamma)).

Any of penalty, lambda, or gamma with length 1

is recycled to this common length.

References

Candès EJ, Wakin MB, Boyd SP (2008).

“Enhancing Sparsity by Reweighted \(\ell_1\) Minimization.”

Journal of Fourier Analysis and Applications, 14(5), 877–905.

doi:10.1007/s00041-008-9045-x

.

Fan J, Feng Y, Wu Y (2009).

“Network Exploration via the Adaptive LASSO and SCAD Penalties.”

The Annals of Applied Statistics, 3(2), 521–541.

doi:10.1214/08-aoas215

.

Fan J, Li R (2001).

“Variable Selection via Nonconcave Penalized Likelihood and its Oracle Properties.”

Journal of the American Statistical Association, 96(456), 1348–1360.

doi:10.1198/016214501753382273

.

Frank LE, Friedman JH (1993).

“A Statistical View of Some Chemometrics Regression Tools.”

Technometrics, 35(2), 109–135.

doi:10.1080/00401706.1993.10485033

.

Friedman J, Hastie T, Tibshirani R (2008).

“Sparse Inverse Covariance Estimation with the Graphical Lasso.”

Biostatistics, 9(3), 432–441.

doi:10.1093/biostatistics/kxm045

.

Fu WJ (1998).

“Penalized Regressions: The Bridge versus the Lasso.”

Journal of Computational and Graphical Statistics, 7(3), 397–416.

doi:10.1080/10618600.1998.10474784

.

Tibshirani R (1996).

“Regression Shrinkage and Selection via the Lasso.”

Journal of the Royal Statistical Society: Series B (Methodological), 58(1), 267–288.

doi:10.1111/j.2517-6161.1996.tb02080.x

.

Wang Y, Fan Q, Zhu L (2018).

“Variable Selection and Estimation using a Continuous Approximation to the \(L_0\) Penalty.”

Annals of the Institute of Statistical Mathematics, 70(1), 191–214.

doi:10.1007/s10463-016-0588-3

.

Wang Y, Zhu L (2016).

“Variable Selection and Parameter Estimation with the Atan Regularization Method.”

Journal of Probability and Statistics, 2016, 6495417.

doi:10.1155/2016/6495417

.

Zhang C (2010).

“Nearly Unbiased Variable Selection under Minimax Concave Penalty.”

The Annals of Statistics, 38(2), 894–942.

doi:10.1214/09-AOS729

.